The Day the Gold Disappeared

by Carl Hegelman

In the long summer vacation of 1971, I “worked” on a construction site in the English countryside where they were proposing to build a new hangar for the U.S. Air Force, and used the proceeds to take a holiday in Greece with my friend Charles. Originally, the idea had been to hitchhike, having crossed the channel on the boat and made our way from Calais to Paris by bus. We soon found out what I had been warned of, that the French can’t abide hitchhikers. After sleeping in the Bois de Boulogne we fluked a short ride to a small town by the name of Auxerre, and there our luck ran out. We stood by the side of the road and for the rest of the day stuck out our thumbs in vain. There was a storm that night, the worst they had suffered for many years, and, abandoning the woods, we laid down our dampened sleeping bags on a narrow strip of shelter by the pumps under a gas station canopy which rang all night with the fusillade of golf-ball sized hailstones. Having stood by the side of the same road for most of the next day, we got tired of looking up Gallic nostrils and spent some precious money on train tickets to Dijon (in the south, named after the mustard). Amazingly, even after dark, we got a lift from the eastern outskirts with some clergymen — they were Belgian, not French — stayed the night for free at their monastery in the mountains, and arrived in Lausanne the next day full of warm feelings for les Belges. The Swiss, too, were much less snooty than the French, and it took no more than a couple of hours to get to the border town of Brig, where we were picked up from the Shell station at the foot of the nearby Alp by a truculent Italian workman in a Fiat, who drove us to Bologna without a word. And that’s when Richard Nixon stepped in. He decided to take the U.S. dollar off the gold standard, and as a result, for a couple of days, nobody would change any money. All you could get in the cambio for your travellers’ cheques or your leftover francs were Italian shrugs.

If you’d asked me at the time why the bureaux de change had shut down, I’d have had absolutely no clue, nor did I spend any time wondering about it as we wandered, hungry, about various piazze looking for somewhere to get lire. The fact that my holiday had been financed by the U.S. Air Force didn’t occur to me as being in any way related. But the “Nixon Shokku”, as the Japanese called it, was a historic event. It marked the end of the Bretton Woods international currency system put in place by a passel of politicians and economists at a conference in New Hampshire some 27 years before, in 1944.

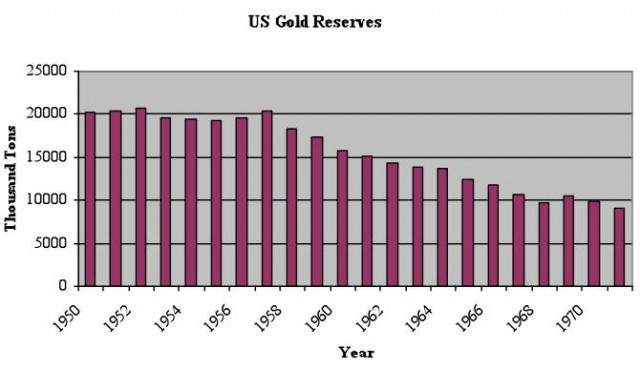

The idea of Bretton Woods was to create stable exchange rates to facilitate international trade and forestall the competitive devaluations that had helped destroy it in the 1930s. The way they did it was to fix the dollar to gold (at $35 per ounce) and fix all the other currencies against the dollar, so anyone wanting to do business with another country would know how much it was going to cost him. If you were a foreign central bank, you could, if you wanted, convert your dollars into gold, so really every major currency was indirectly tied to gold. The U.S. at that time owned about 65% of the world’s gold reserves, and was required by the Federal Reserve Act to allow no more than four times that amount in circulating dollars. Most of the dollars, obviously, were owned by Americans, and Americans weren’t allowed to convert their dollars into gold — in fact, it had been illegal since 1933 for Americans even to own gold other than in jewelry or numismatic coins. So nobody had much doubt that if he wanted gold instead of dollars the U.S. was good for it, and so nobody really bothered converting their dollars to the less convenient gold. Bretton Woods also created the IMF, whose job was basically to make sure the member countries didn’t endanger their exchange rates by irresponsible spending — a sort of international “fiscal union” much like what they’ve been talking about recently in Europe.

As proprietor and printer of the world’s reserve currency, the U.S. wasn’t behindhand in spreading it abroad. There was the $13bn Marshall Plan, which, together with $12bn in previous aid, revived Europe and so created markets for U.S. goods. (This may not sound like much now, but bear in mind, U.S. GDP at the time was between $220bn and $270bn, and the entire Federal budget in 1948 was about $30bn.)

Then there was a lot of spending on military bases and a flood of foreign investment by U.S. corporations building up their international operations. Still, people didn’t really start to worry until the late 1950s. Beginning in 1959, there was a distinct tendency for the foreign central banks, suspecting the dollar was overvalued, to show up at the “gold window” and demand gold for their increasing piles of dollars. Vietnam and the Great Society programs didn’t help: The Federal budget more than doubled from 1960 to 1970. The amount of freshly minted dollars grew so much that, in 1968, Congress had to repeal the law restricting circulating dollars to four times the gold reserves, allowing the U.S. Treasury to keep printing. Which, of course, worried the foreign central banks even more. When foreign finance ministers whined about the growing level of dollar-induced inflation, Nixon’s Treasury Secretary, John Connally, famously told them the dollar “may be our currency but it’s your problem.” (Yes, the same Connally who got shot in JFK’s Dallas motorcade. By some accounts, he was also, indirectly, indispensable to the election 30 years later of George W. Bush.) Not surprisingly, the foreign central banks kept coming. By 1971, U.S. gold reserves were down from 65% of world reserves to 25%. Nixon was facing re-election in 1972 with unemployment and inflation at vote-squashing levels, and the overvaluation of the dollar tied to gold — though it had been an immense boon to U.S. corporations by enabling them to buy foreign assets on the cheap — was crimping his ability to stimulate the domestic economy.

And so it all snapped that August. Allegedly, it was triggered by a British request to reactivate the Fed’s swap lines and cover hundreds of millions of dollars they had absorbed in keeping the markets orderly. These swaps were essentially a guarantee against loss due to dollar devaluation and had been used for years to prevent too much depletion of the US gold reserves.

Connally, however, told Nixon it was a request for $3bn in gold — about a quarter of the remaining U.S. reserves — a story repeated by Nixon in his memoirs. “All Connally had to hear was that some limey wanted gold,” according to Charles Coombs, a New York Federal Reserve official, and his mind was made up. Connally persuaded Nixon to default on Bretton Woods and put the blame on “an assault by international speculators” — the European and Japanese. They didn’t even tell the Chairman of the New York Federal Reserve. And certainly not the fiscal police, aka the IMF. For good measure, Nixon also imposed a 10% surcharge on imports. Politically and economically, the default and attendant measures turned out to be a brilliant move.

No wonder there was deadlock in the cambio. Suddenly, nobody knew what the exchange rates should be. How many lire for your French francs? Shrug. We were a little weary of hitchhiking by this time, stuck in Bologna on a rainy Sunday evening with too much baggage, no map, no phrase book, not a word of Italian and no clue how to find the road south to Brindisi, where you could catch a ferry across to Corfu and Greece. Fortunately, Charles, who was a worried, conscientious sort of bloke, had taken the precaution of buying some lire before we set off from London. It wasn’t much, but enough to get us on a decrepit wooden-benched train as far as Bari, about sixty miles short. Bari, across the Adriatic from our goal, turned out to be an exceptionally desolate, parched little seaside town, with oil storage tanks and threatening-looking yobs in tight trousers. We spent our last few lire, after sweatily debating in the August sun, on a delicious-looking iced drink which turned out to be all but undrinkable. (All flash, these Italians, Charles decided). Fortunately, the Nixon shock soon passed, the money-changers became more affable, and, a few spaghetti bologneses later, we found ourselves in Athens, camping on the roof of the Hotel Sans Rival. It was mobbed with fellow travellers attracted, like us, by the price — about 5p (roughly 11 cents) a night¹, as I recall. You could share a room for about 25p, but only Americans could afford that, and the roof was wall-to-wall sleeping bags and European longhairs, transients en routeto and from the islands via the port at Piraeus.

All in all, it wasn’t a great trip. We got stuck in a lift for an hour in Athens in the middle of a blazing heatwave. On the ferry over to Mykonos, someone on the deck above puked on my head and there was nowhere to wash my then-copious hair. I didn’t even meet any girls, let alone find a Shirley Valentine type romance. For a ridiculous technical reason, few of the photographs I took with my prized 35mm Voigtländer rangefinder came out. Really, overall, a bit of a bust.

Forty years on, with Greece and Italy threatening to throw the international banking system into fresh turmoil, there is some added resonance to this little episode. The Greeks now owe a lot of Euros which they have no means to pay. A lot of that debt is held by Greek banks, which means that those banks are effectively bust. The Greeks themselves are very sensibly withdrawing Euros from their accounts, which puts those banks in a very tight spot. Quite a lot of the Greek debt is owned by German and French banks, so their ability to lend is severely curtailed, exacerbating an ongoing credit crunch which will undoubtedly provoke a recession in Europe next year. Then there’s the problem of the Credit Default Swaps (CDSs), which are essentially guarantees of the Greek debt. Nobody seems to know who undertook those guarantees (AIG? Goldman?) or how much is outstanding, but if the Greeks default (and there’s a very indignant debate about what “default” means here) they’ll be on the hook for the difference between the actual value of the Greek debt and its face value. The shakiness of the German and French banks, together with the CDS threat, may in turn endanger the US banks. (You can play this by buying one of the short financial ETFs, like SKF, with the risk that they might default too.) And then there’s the possibility that the same thing will happen to Italy and Spain, whose debt is much more ginormous than the paltry Greek debt. The debacle has already claimed one U.S. victim — Jon Corzine’s MF Global, which had $11.5 billion of Italian, Spanish, Belgian, Portuguese and Irish debt (hedged down by some unfortunate counterparty to $6.4bn) — with knock-on effects to its lenders.

Angela Merkel, the German premier, must surely see an opportunity here to put Germany, de facto, at the head of a fiscally integrated European Union with legal authority by treaty over all Euro country budgets. The Brits threw a spanner in those works with their recent veto of the proposed treaty. Nicolas Sarkozy, in France, is wary of full fiscal union, perhaps because France might become its victim if its credit rating is cut, but would still like the EU to have enough clout to make sure the Greeks pay the French banks what they owe. The European Central Bank, which is like the Fed only without the accompanying ability to control national budgets, is ostensibly refusing to come to the rescue by being a lender of last resort. (Except maybe through a back door: its wily new chief, Mario Draghi, is, after all, a former managing director at Goldman Sachs). The Europeans are left with a relatively small “stability fund” (joke!) and our old friend the IMF.

The Greeks have an overvalued currency but no ability to become more competitive through devaluation, except by abandoning the Euro, which would leave them just as poor but without any of the huge advantages of sharing a common currency. (Imagine a United States where you had to change currency, at some unpredictable rate, every time you transacted across state lines). The fiscal police, which in this case means the various European financial authorities as well as the IMF, are only willing to bail them out if everybody tightens their belts. The Greek government, without getting any definitive consent from the Greeks, has agreed to sell off the country — or at least much of its transportation, utility, energy, telecomm, gaming and real estate assets — to foreign (read German/American?) interests in order to help pay their debts.

In short, the Greeks are kind of in the same spot as the U.S. was in 1971, only without the massive economic clout which forces everybody else to forgive them.

But you might as well be poor in Euros as poor in New Drachmas. Even if the EU throws them out, there’s nothing to stop the man in the street using Euros, or, pace Gresham, having dual currencies (like, say, Zimbabwe). Putting myself in the shoes of the average Greek, I’d be inclined to do what Nixon did: Default and everybody can go to hell.

¹ By my calculation, adjusted for inflation that would be about 57p today, or around 60 to 90 cents, depending on how you do it.

Carl Hegelman (a pen name) is a corporate bond analyst and a connoisseur of leisure.