There Is No College Bubble

by Malcolm Harris

If you visit collegedebt.com, that’s exactly what you find. It’s a stark display, black on white, with an ominous ticker counting up. “Current student loan debt in the United States.” Right now it’s at $1.339 trillion, but by the time you read this, the sum will be larger. The site is owned and operated by self-styled maverick billionaire Mark Cuban, who uses it to drive home a point he makes whenever the media will listen: American higher education is overpriced, and the bubble is going to pop.

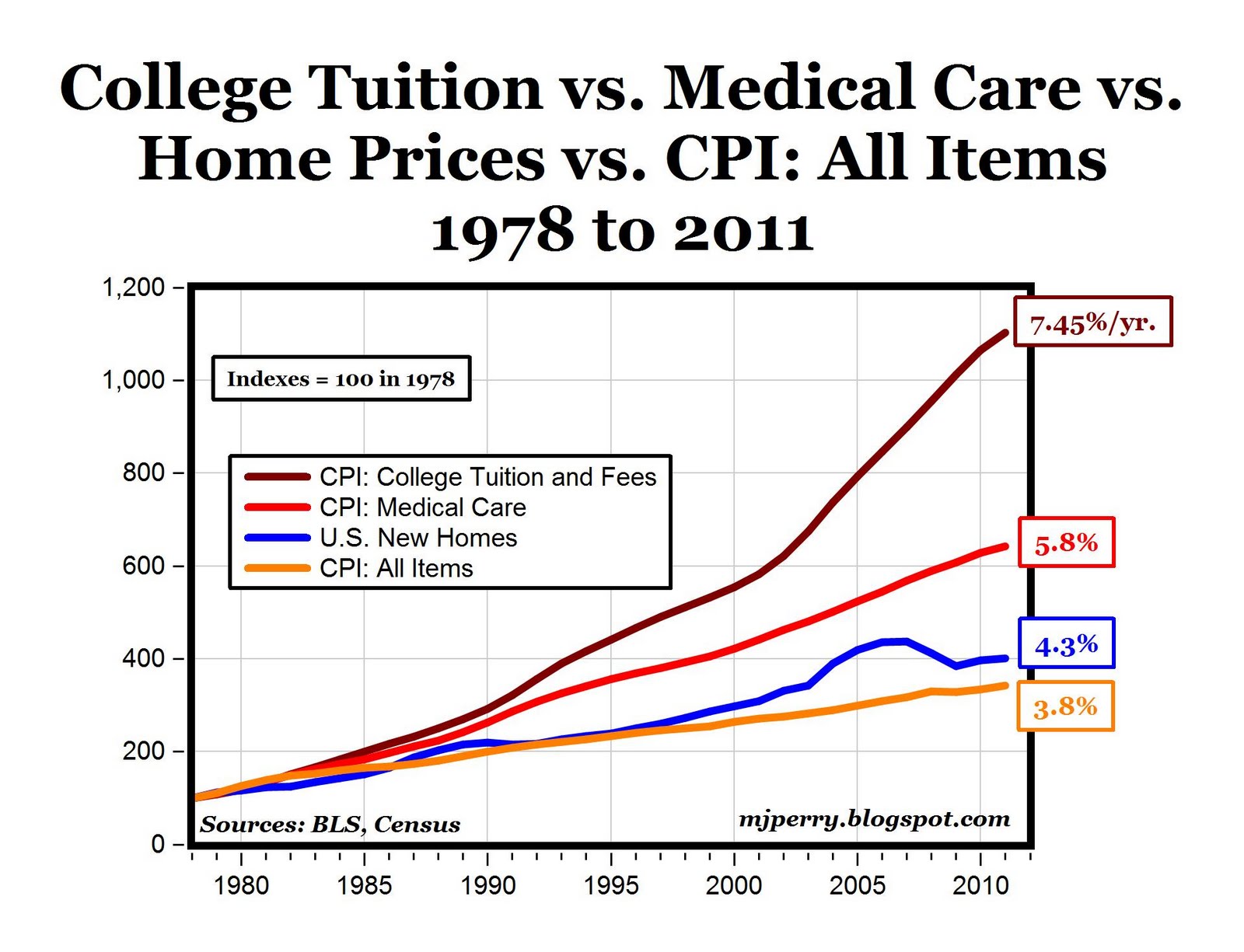

Higher education has been pegged as the next bubble since the 2008 housing crisis, and the evidence is compelling. Increases to university tuition and fees outpaced both pre-crisis housing prices and climbing healthcare costs. The growth over the last 35 years certainly looks unsustainable when you plot it on a graph, and America remembers what happens when an asset bubble collapses. But it’s been seven years since the housing crisis, and while new home prices dipped, tuition and fees haven’t really. College costs have sustained more public scrutiny — the cure for bubbles — than real estate ever did before the crash, and still no pop. The average undergraduate now takes out $30,000 in loans. Universities keep expanding, building new facilities and introducing all sorts of auxiliary services. Despite omens to the contrary, the higher education industry is going strong. Analysts are waiting for the bubble to pop; this is the story of why it won’t.

{kind=link}

The real estate bubble was able to expand because lenders assumed that prices would increase indefinitely. After all, God isn’t making any more land; scarcity is built into the asset class. As long as prices kept growing, it didn’t matter much if buyers could really afford the houses they wanted. If owners defaulted, then the banks would take possession of a property whose value had increased since the original sale. It was a no-lose proposition, and in our advanced market culture, firms will pursue no-lose propositions to and beyond the full extent of the law. Banks hedged their loans by making more loans in different regional markets, protecting themselves from everything except a simultaneous nationwide deflation in housing prices.

Of course, simultaneous nationwide deflation in housing prices is exactly what happened. As homeowners found themselves owing more on their properties than they were worth, they defaulted. The robust housing market was gone in the blink of an eye, and lenders were stuck holding the bag — at least until they passed it to the taxpayers. Bailouts stopped the bleeding, home prices recovered, and now they’re growing again, albeit with moderated exuberance. It was a close call for the American economy, and neither lenders nor borrowers are looking to repeat the mistake.

But money managers are always trying to get their risk down to zero on paper. Zero risk means free money, and everyone likes free money. When it came to student lending, the federal government was happy to help. With the Higher Education Act of 1965, Congress created the Federal Family Education Loan Program. The FFELP made lending to a high-risk population as risk-free as possible. Under the program, private firms still lent their capital, but they were subsidized and backed by the Treasury, and in the event of defaults, the government promised to pay up with interest. It was an irresistible deal for commercial lenders, which was the plan. Providing credit for college students while they expanded their minds was deemed in the public interest.

At the initiation of the FFELP, total tuition, fees, room, and board at public four-year universities averaged $950, $1907 at private. It wasn’t nothing, but a summer job made it manageable for independent young people. The largest cost for prospective college students in 1965 wasn’t tuition — it was not working. There were jobs for high school graduates, and the wage premium for the college educated was less than half of what it is now. With a mere $1000 annual advantage for workers with degrees (in 1965 dollars), it would take them a long time post-graduation to make up for $17,000 in pay foregone over four years in school. There simply did not exist, at the time, the same near-term financial incentives for young Americans to attend college. Cheap credit just for being a student was a national policy meant to pull more people into school, and it worked.

Job training outside primary and secondary school had been in the purview of employers, who were forced to pay for the development whatever skilled labor they needed. But competing against the Soviet Union, American economists and policymakers became concerned with the condition of the national “human capital stock.” Without a push from the government, private incentives alone might not produce the world’s most advanced labor force. Between 1965 and 1975, the number of enrolled students doubled, from six to 12 million. It was a huge national investment in the future of labor, by the government, by commercial lenders, by families, and not least of all, by students themselves.

This influx of new college students was not a bubble, and most of them had no cause to regret their decision to attend. The gap in wellbeing between graduates and other workers was growing rapidly, and forward-thinking young Americans didn’t want to be left behind. Enrollment increased steadily, but in the early eighties, higher education tuition, expenditures, and loans started inflating in a bubbly manner. In the decade between 1971 and 1981, tuition at public and private colleges actually decreased by a small amount when adjusted for inflation, but in the decade that followed, it increased 60 percent at private schools and 56 percent at public colleges. Under the FFELP, private lenders and the government worked together to ensure that regardless of these costs, more and more students could still afford to go to college. The whole machine continued to hum along according to plan. Workers got educated, lenders made profit, GDP increased, America remained competitive.

But by the late eighties, some conservatives worried that the government had inadvertently created a complex system of price mismanagement. In a 1987 op-ed for the New York Times called “Our Greedy Colleges,” Ronald Reagan’s Secretary of Education William J. Bennett advanced the idea that universities were raising prices because they were over-subsidized. If the government offered more grants and loans, then schools would feel safe raising fees without having to worry about pricing out too many students. As long as enough well-qualified applicants could still manage the cost, colleges would use the additional revenue to expand and compete with other schools for market position and prestige. This idea became known as the “Bennett Hypothesis.”

As a small-government conservative, Bennett didn’t think the taxpayers should be in the business of increasing higher education access, but Americans disagreed; annual federal support to undergraduate students (grants and loans) swelled from $42 billion in 1990 to $194 billion in 2010. (table 3a) The feds also encouraged corporations and wealthy individuals to collaborate with universities in the form of tax breaks and incentives. The Bayh-Dole Act of 1980 allowed universities to begin patenting ideas that result from government research grants. Nurtured by a trough of easy credit borrowed by other people, American universities grew and grew. Expenditures rapidly outpaced enrollment: Public and private schools spent a combined $275 billion in 1990 (in 2012 dollars), which nearly doubled to $500 billion by 2012.

The growth in college spending and debt over the past 25 years triggers the bubble alert. There is no clear reason why educating people should have become that much more expensive. The market mechanism for the allocation of human capital seems to have gone haywire. Everything associated with college has seen its costs rise: Textbooks, like books in general, should be facing price competition from e-books, but between 1998 and 2014, the cost of textbooks rose 161 percent, 115 points above the Consumer Price Index and 162 percent above recreational books. Higher education costs of all sorts are responding to their own set of market pressures, forces divorced from regular inflation.

{kind=link}

If you walk around an average American university campus, it’s easy to see where some of the money is going. Colleges are nice. That’s a change that, for many of them, has happened recently. Universities complete and begin $20 billion a year in construction, and 60 percent of it is for new buildings. Not only are schools always working on new facilities, the median cost per square foot on these projects has skyrocketed: Tripling between 1997 and 2012 for academic and science buildings, quintupling for residential halls. It’s the way institutions spend when money is not an obstacle, when the cash they’re shelling out belongs to other people. But at the end of the day, the money has to come from somewhere.

In the 2013–2014 school year, the typical out-of-pocket higher education cost was about $14,000. Few students and families can pay for college without loans — even the typical high-income family took out $5000 in education debt. Still, two-thirds of costs are paid at the time they’re incurred. Parents at all income levels dedicate thousands of dollars a year to college education, and so do the students themselves With 20 million college students, the yearly family, friends, and student cash contribution to higher education is around $200 billion, which is equivalent to the gross domestic product of Algeria. This is real money — a lot of money — that Americans have already labored for.

Despite their nation-sized collective offering, most students and their families (about 80 percent) are not able to pay the full price for higher education upfront. Seventy percent of students will graduate with debt. Under the FFELP, these loans were made by commercial institutions, but there was no real reason for the government to go through middlemen lenders since the state was backing the contracts anyway. As a cost-saving measure included in the 2010 Affordable Care Act, the Treasury cut out the private firms and assumed direct responsibility for the vast majority of student lending. The government nationalized the student loan industry, but no one much noticed.

When Congress agreed to phase out the FFELP to help offset the costs of Obamacare — a good way to keep Republicans from arguing — the commercial lenders disappeared, as did much of the market for Student Loan Asset Backed Securities. The private industry vanished more or less overnight. And when the Department of Education woke up alone, they found themselves surrounded by billions and billions of dollars.

The thing about student lending is that it’s profitable, especially for the Treasury, which borrows as much money as it wants at virtually no cost. In the three years between 2012 and 2014, the Department of Education’s loan program pulled in $107 billion in profit, putting it right between Apple and Exxon as the second-highest earning US firm.

This means that as fast as the Treasury is originating loans ($107 billion in 2015), borrowers are paying them back faster. Yet the outstanding total keeps growing. This phenomenon should be familiar to anyone born this side of 1545, when Henry VIII legalized interest-bearing loans. Undergraduate borrowers in 2015 will face 4.29 percent interest. If a borrower took out $30,000 and paid it back promptly at $307.89 a month over the standard 10-year period, they would end up paying a total of $36,946.40, a solid return for the government. And that’s if they’re prompt — borrowers who take longer pay more as interest piles up. Do that 40 million times a year, and student lending turns out to be a very lucrative business.

Why, if student lending is such a profitable industry, did the private banks cede their market share without a fight? When a teenager starts borrowing tens of thousands of dollars for school, they don’t necessarily have any collateral that the lender can repossess. If you lend someone money for a car or a business, there’s a car or a business to seize. But human capital is inalienable. No lender can repo your sociological methods course, or even your diploma (at least not yet, though the technology is imaginable). This led the architects of the Higher Education Act to worry. What if someone were to take out a full basket of medical school debt, declare bankruptcy at graduation, and enter the high-paying field debt-free? What if a million someones were to do it? As part of the Bankruptcy Reform Act of 1978, Congress made student loans non-dischargeable. Once you take out student debt, the law ensures you’re stuck with it.

The student loan system works very well if the government is doing the lending: The Treasury doesn’t have to balance its books; the state can wait indefinitely to be paid back without worrying about solvency. Just as importantly, the government collects with the power of the state. They make the law, and they can exempt themselves. Courts have held that, for example, that the Fair Debt Collections Practices Act doesn’t apply to agents of the federal government, leaving them free to collect debt unfairly. The Higher Education Act even allows the state to garnish borrowers’ wages and tax refunds. With total stability and exceptional collections capabilities, the government can ensure that no matter how big the higher education bubble gets, it won’t pop.

How do the pessimists imagine things will go wrong? Mark Cuban thinks that students will eventually refuse to take out increasingly sublime loans, which will force colleges to reduce prices beyond their abilities, leading them to implode. But so far, this decline in demand hasn’t happened. A college degree is still worth what colleges say they’re worth, and then some. The wage gap between college graduates and high school graduates was $17,500 a year in 2013. If schools and the state required/invited students to take out $60,000 or $120,000 in student debt, the demand would still probably be there, especially if schools are allowed to accept elite teens from all over the world and the federal government continues to extend loan-repayment periods.

Between loan repayments and tuition checks, Americans are spending around $325 billion annually on college education, not including debt or taxes. Even if the tuition rates decelerate, that count will increase. And yet, the system works. It works for the government and it works for employers and it works for universities and it works okay for most college graduates, at least compared to the alternative.

The truth is that, although the college wage premium has increased in the past three decades or so, it’s not because young graduates are on average better off. Between 1986 and 2013, their median real annual earnings increased by less than $800. But over the same period, for those with no college, real earnings dropped by $2,525. The economic choice this country poses to young people about higher education has stopped being about opportunity for wealth — now it’s about fear of poverty. Empirically, the latter is a more effective motivator. Whether or not this is an appropriate way to produce educated workers is, in theory, a question for our democracy.

Despite being apocalyptic, the Higher Education Bubble narrative is in some ways comforting. It takes away political questions like, “Why does a public university spend $150 million on an athletic complex?” or “How many hours of work should it cost someone to go to college?” and replaces them with practical ones like “What are the best precious metals to horde?” If there’s a bubble, then the giant pile of debt isn’t real; one of these days it’s going to disappear. The unknowable disaster is preferable because the problem will, one way or another, solve itself. But it won’t, because there is no problem. Instead, there is a system that reliably turns future labor into spending today, and at an interest rate pegged above government borrowing costs. If we had a bubble, we wouldn’t have to confront the fact that Americans have already sold and spent billions and billions of hours of their yet unrealized lives, and they’re going to have to pay.

The collegedebt.com ticker is at $1.342 trillion now. At the median wage for young college graduates that’s 60 billion hours, or 37.5 full-time weeks of labor per outstanding borrower. When you read this, it will be higher.

Photo by Catherine LaRocca